Homeowners Insurance Crisis in Florida 2026: What's Happening Now?

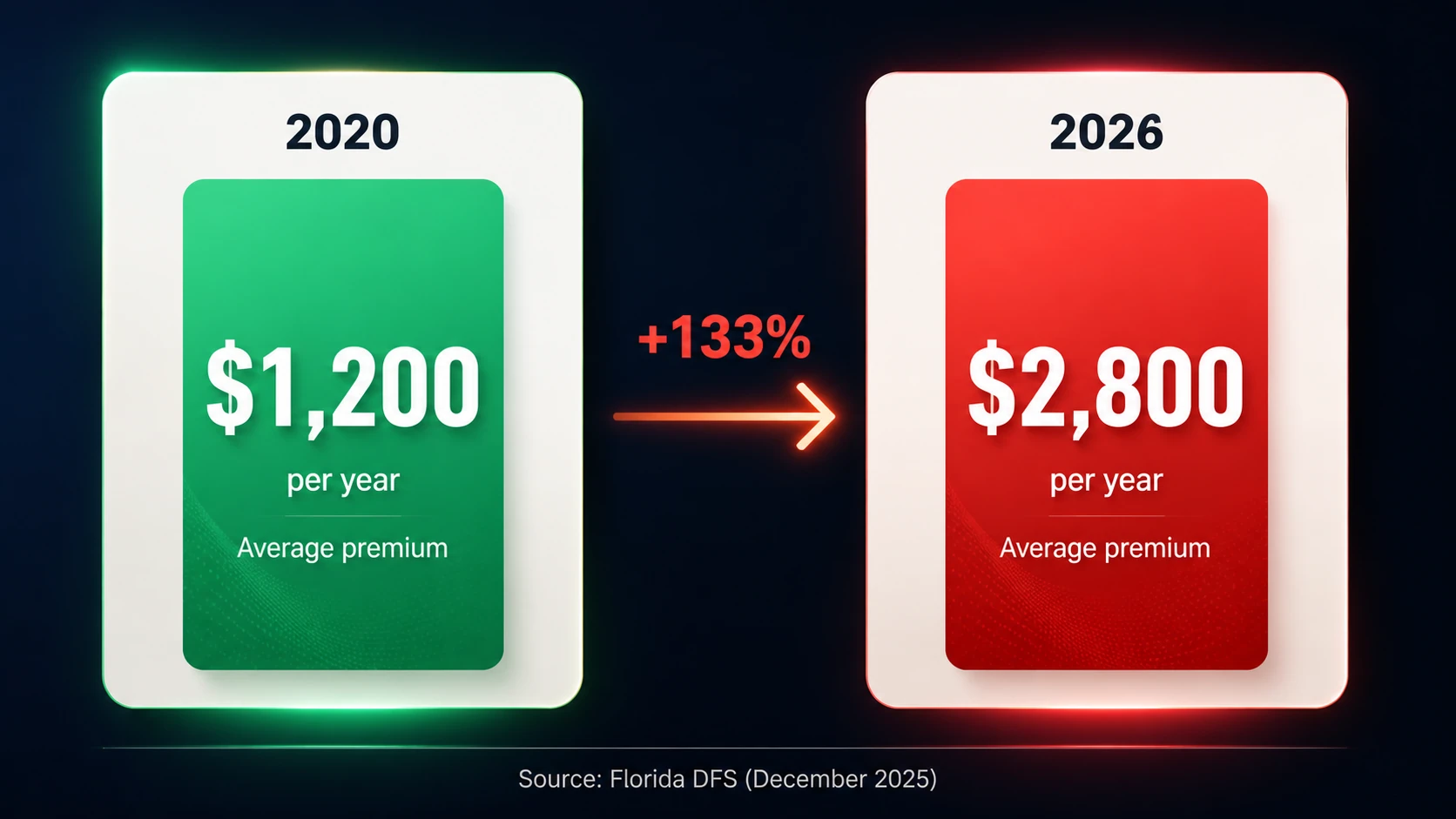

Florida's homeowners insurance crisis has reached a critical point. In 2026, thousands of homeowners face premiums rising 20–40% year after year, or simply cannot find coverage. Why is this happening? What should you do now? This guide explains it clearly.

Source: Florida DFS, December 2025

What's Happening with Home Insurance in Florida?

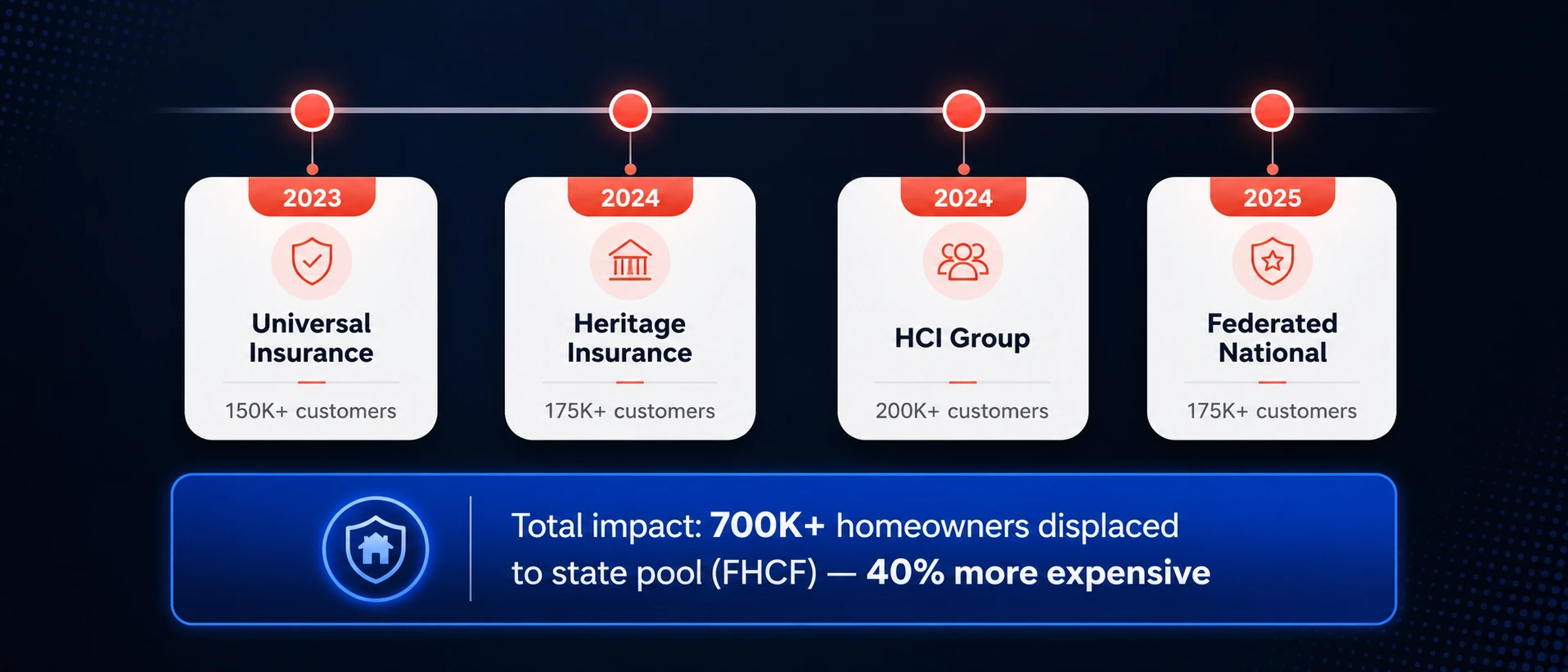

Over the past 24 months, four major insurance carriers have completely exited Florida's market:

Result: 700,000+ homeowners had to find coverage through smaller companies or Florida's state insurer of last resort, the FHCF (Florida Hurricane Catastrophe Fund), which charges 40% higher premiums.

Florida DFS Data (December 2025)

Why Are Carriers Leaving Florida?

The main reason: water and mold litigation lawsuits. Insurance companies lost $2.3 billion in 2024 due to water and mold damage claims. Trial attorneys in Florida exploited a legal loophole: any water loss, no matter how small, could become an expensive mold claim. Many insurers simply couldn't sustain that financial risk — they exited the market.

Result: less competition means higher costs for you.

Four carriers exited 2023-2025, displacing 700K+ homeowners

Why Does This Matter to You?

If you own a home in Florida, this means three concrete things.

1. Your Premium Will Rise Year After Year

Without competition, carriers can raise prices without losing customers. You have no easy alternatives. Real example — Tampa homeowner with a $300K home:

Total increase over 6 years: 167%. And that's conservative.

2. Fewer Options = Less Bargaining Power

Three years ago, switching carriers was easy. Today, if your home is in the FHCF (state pool), private carriers have very strict criteria:

If you don't qualify, you're stuck in the state pool.

3. Limited Coverage in the State Pool

The FHCF is the "insurer of last resort." It has limits that private carriers don't:

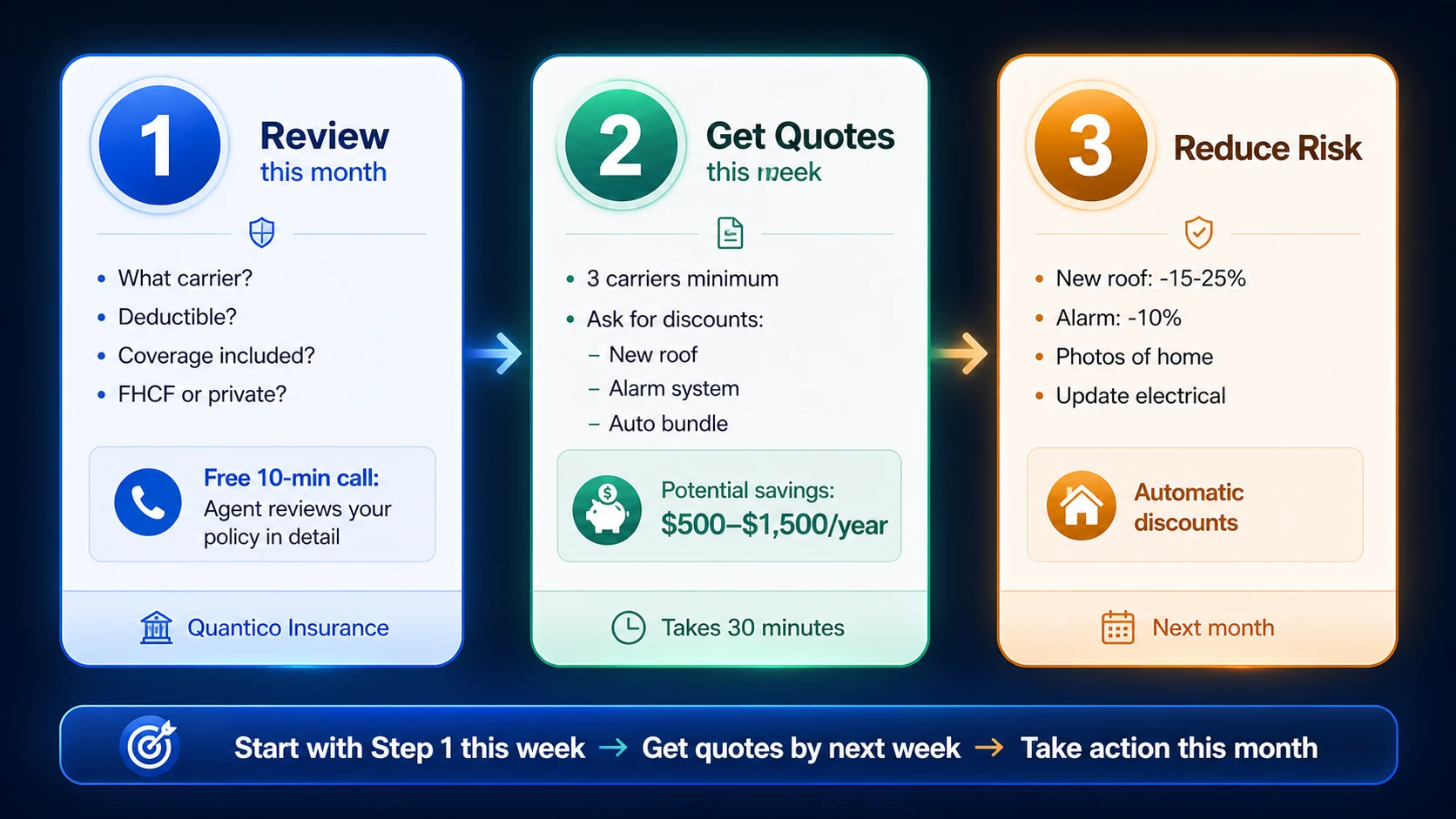

3 Things You Can Do Right Now

Start this month, quote next week, act within 30 days

Step 1: Review Your Current Policy (This Month)

Open your current policy (or call your agent) and verify these 4 key points:

If you're unsure, it's time to talk to an agent. Quantico Insurance offers free policy reviews — about 10 minutes on a call and you'll know exactly what you're covered for.

Step 2: Get Quotes from Other Carriers (This Week)

Don't wait for your policy to renew. Rates change every month in Florida. Right now:

Switching carriers can meaningfully reduce annual costs. It usually takes around 30 minutes to gather quotes.

Step 3: Reduce Your Home's Risk (Next Month)

If your home is "high-risk" to carriers, improve it. Any upgrade can lower your premium:

Frequently Asked Questions

What if I really can't find private coverage?

You have the legal right to FHCF (state pool). But it's more expensive and more restrictive. The key is not to wait — get quotes now while you have options before defaulting to FHCF.

Is flood insurance included in homeowners?

No. Flood is a completely separate policy you must buy: NFIP (National Flood Insurance Program) or private flood insurance. If you have a mortgage in a flood-risk zone, it's mandatory. Even without a mortgage, it's strongly recommended in Florida.

When's the best time to switch carriers?

Now. Don't wait for renewal. A new carrier can take over your policy any time of year — you don't have to wait for renewal.

Which carrier is "best" in Florida?

There is no single "best" — it depends on your specific city, the age and construction of your home, your claims history, and your risk zone. This is why getting 3 quotes is essential.

Next Steps

You don't need to do everything today. But you do need to start:

At Quantico Insurance, we do this every day. We help review which carriers are still open in your area, which discounts may apply, and how to compare homeowners insurance options. When you're ready, request a free quote and an agent will walk you through your options. Final eligibility and pricing depend on underwriting and policy terms.

Related Articles

FMCSA Motus 2026: What Florida Trucking Carriers Need to Know

FMCSA is launching Motus, the new USDOT Registration System. Learn how it affects Florida trucking carriers, USDOT updates, MC authority, insurance filings, BOC-3 and identity verification.

FMCSA Changes 2026: What Owner-Operators in Florida Need to Know

2026 FMCSA updates affecting owner-operators in Florida. Learn what changed with medical exams, safety scores, and insurance costs.