Homeowners Insurance Florida 2026: A–F Coverage Guide

Key takeaways

In Florida, homeowners insurance is no longer an automatic renewal — it has become one of the most important financial decisions for any property owner. After years of rate hikes, cancellations and market changes, 2026 brings signs of stabilization, more competition and some rate reductions, but that does not mean every policy is well configured.

For many homeowners in Orlando, Kissimmee, Winter Haven, Clermont, Jacksonville, Melbourne and other Florida cities, the question is no longer just "how much does it cost?" but "what am I really paying for, and what does my policy cover if a hurricane, fire, theft, lawsuit or loss of use happens?"

In this guide from Quantico Services LLC, we explain what is happening in the market, why it matters for your wallet, and how to review the A–F coverages of a homeowners policy before you renew or quote.

What is happening with homeowners insurance in Florida?

Florida is coming off difficult years driven by hurricanes, litigation, expensive reinsurance, insolvencies and carrier withdrawals. In 2025–2026 there are signs of stabilization: flat or reduced filings, more competition and reduced Citizens exposure. To be clear: "stabilization" does not mean everyone will pay less — it means the market is healthier than it was two years ago.

Mini market timeline

Why it matters to you as a Florida homeowner

What happens with your homeowners insurance can affect your mortgage escrow, annual premium, hurricane deductible and lender requirements. A serious review can also reveal important gaps: low dwelling limit, limited personal property, insufficient liability or missing flood insurance.

A few local examples:

Before vs. now

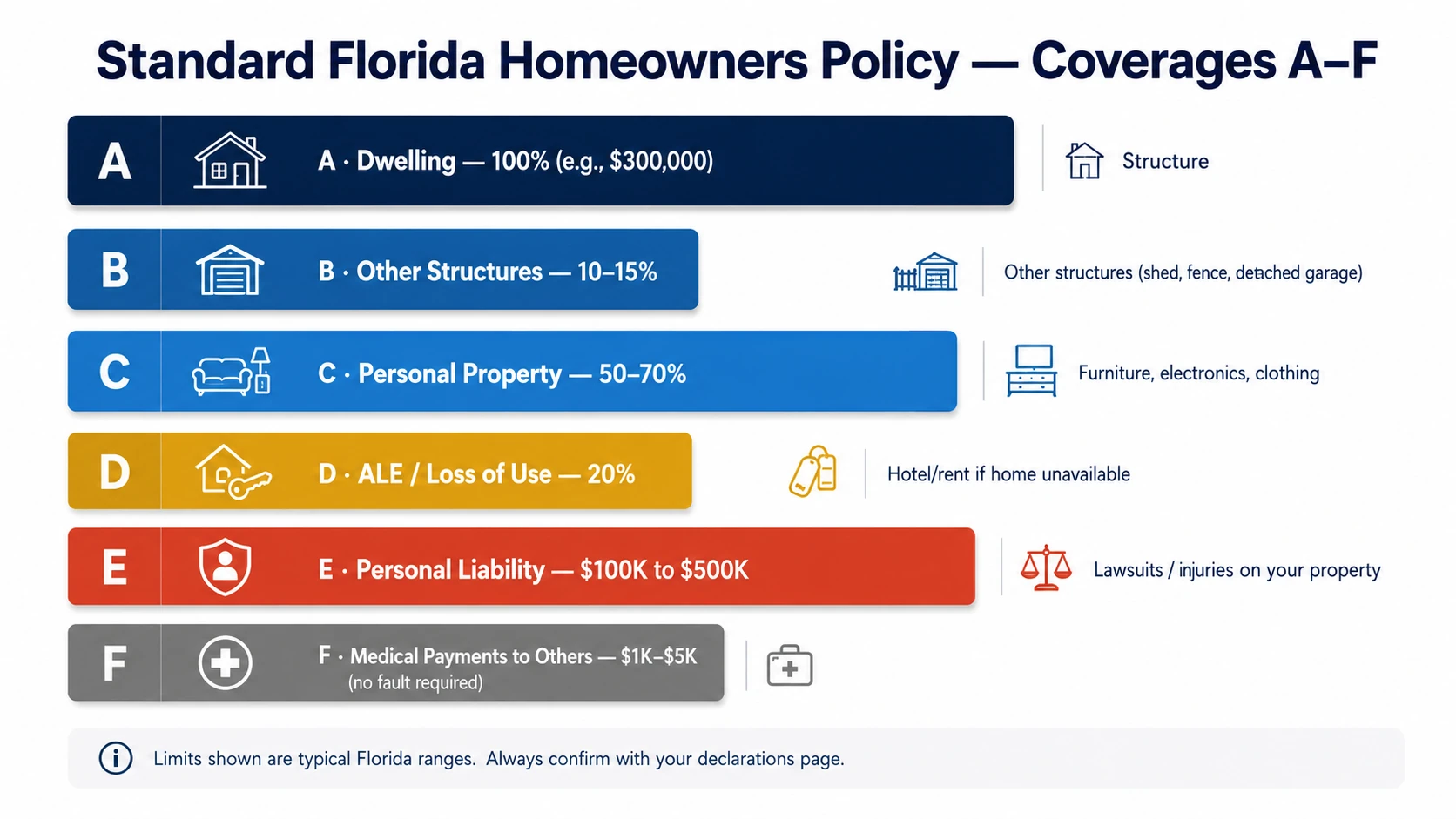

What a standard homeowners policy covers: A–F

A standard homeowners policy is typically organized by coverages. The letters A–F help you understand which part protects the structure, your belongings, temporary expenses and personal liability. Percentages and limits vary by carrier, location, property and declarations page.

The limits shown are typical ranges. Always confirm the actual amounts on your declarations page.

Coverage A — Dwelling

Protects the main structure of the home: walls, roof, built-in systems and permanent fixtures. It is usually the base for calculating other coverages. Make sure the limit reflects replacement cost, not just market value.

Coverage B — Other Structures

Protects separate structures such as fences, sheds, detached garages or gazebos. Many policies calculate it as a percentage of Coverage A, but it can vary.

Coverage C — Personal Property

Covers furniture, clothing, electronics and other personal belongings. Review sublimits for jewelry, special equipment, tools or high-value items.

Coverage D — ALE / Loss of Use

Helps with additional living expenses if your home becomes uninhabitable due to a covered loss, such as hotel or temporary rent. It does not apply to every scenario; it depends on the cause of loss.

Coverage E — Personal Liability

Protects against certain claims for injuries or damage to third parties. Many homeowners review whether $100K, $300K or $500K is enough for their exposure.

Coverage F — Medical Payments to Others

May cover small medical expenses for third parties injured on your property, without needing to prove fault, within the policy limits.

Note: Flood insurance, umbrella liability, equipment breakdown, water backup and scheduled personal property may require separate policies or endorsements.

Concrete actions now

Step 1 — Today: review your declarations page

Step 2 — This week: compare options before renewal

Don't wait until the last day. In Florida, some carriers require inspections, photos, roof details, wind mitigation or a 4-point inspection. Comparing with time lets you review deductibles and endorsements without pressure. Renewing soon? Call Quantico at (321) 407-5597 and we'll review your policy with you.

Step 3 — Next month: prepare your property for better underwriting

Frequently asked questions about homeowners insurance in Florida

What is homeowners insurance?

It is a policy that helps protect your home, belongings and personal liability against covered losses. Details depend on the carrier, limits, deductibles and exclusions.

Does homeowners insurance cover hurricanes in Florida?

Many policies include windstorm or hurricane coverage, but with a special deductible. You should confirm on your declarations page whether it applies and how much you would pay before insurance responds.

Is flood insurance included?

Usually no. Flood damage typically requires a separate flood insurance policy. This is especially important in coastal areas and near lakes, rivers or drainage zones.

What is Coverage A?

Coverage A or Dwelling protects the main structure of the home. It is one of the most important limits because it can influence other coverages.

What is Loss of Use?

Loss of Use or ALE can help with hotel, temporary rent and additional expenses if your home becomes uninhabitable due to a covered loss.

Why does my insurance go up even though I had no claims?

It can rise due to rebuild costs, reinsurance, roof age, location, area history, carrier changes or regulatory adjustments.

Can I switch carriers before renewal?

Yes, you can generally compare options before renewal. It's important to avoid coverage gaps and confirm lender requirements if you have a mortgage.

Can Quantico help me in Spanish?

Yes. Quantico Services LLC offers bilingual advice in Spanish and English for homeowners insurance and other lines of insurance allowed in Florida.

You may also be interested in

Sources

Disclaimer: Coverage, limits and availability vary by carrier, property, location and underwriting. This article is educational and not legal or claims advice.

Need a quote?

Our agents are ready to help you find the best coverage.

Obtén una Cotización Personalizada en 2 MinutosRelated Articles

What Is Motor Truck Cargo Insurance? A Simple Guide for Florida Trucking Businesses

Motor Truck Cargo Insurance helps protect freight while it is being transported. Learn what it covers, what it does not cover, and why Florida trucking businesses may need it before hauling loads.

Understanding Your Homeowner Insurance: What's Covered and What's Not

A comprehensive guide to homeowner insurance coverage, exclusions, and how to make sure your home is fully protected.